One question I routinely get asked by friends and readers of this site is, “Can you teach me how to save money without losing track of what it’s for? How do you account for your money when you are saving for an emergency or for a future need?”

The problem boils down to this issue: you have to keep track of what money is to be used for what purpose.

The problem boils down to this issue: you have to keep track of what money is to be used for what purpose.

When you deposit money into your savings account, it gets mixed in with all the other money in the savings account. How do you keep the boys separated and make sure the money designated for the new dishwasher actually ends up going for the new dishwasher and not the car insurance or the baseball card fund?

Like many others, this frustrated me too. But then I remembered something my parents used to do that helped with this. So I took their system and enhanced it for the digital age. It completely fixed my issues and has been a lifesaver ever since.

The Classic Envelop System

In the old days, you might find yourself reaching into the desk drawer, pulling out an envelope and stuffing it with cash. Then you would write on the envelope “Dishwasher Fund” and hide it away in your house somewhere. You’d follow this same process for any other item you’d be saving for including vacations, the health insurance bill, groceries, gas, clothes and hobbies.

This describes the classic envelope system way of saving money. This system keeps all the money in the envelope to which it belongs. It creates a process to make sure the exact money gets used for its intended purpose.

Related Content: The Ultimate Guide on How to Make the Best Monthly Budget

The envelope system is still a valid tool for managing cash payments today. However, we’ve moved into the digital age where most banking is done online, transactions are downloaded to computer programs and apps have been developed to keep track of your spending on the go. Money is more likely to be direct deposited in the bank rather than kept at home in large sums.

Plus, the FDIC insures your deposited money at the bank. The savings money at your home is vulnerable to theft and your urges for an extra large cheese pizza.

For these reasons, I keep all of our savings money at the bank. And right now I’m saving for a multitude of items including an emergency fund, bills, private school for the kids, Christmas, summer vacation, a new to us car and several other specialty funds.

At one point keeping track of all this was confusing. But I developed a system based on my parents classic envelop system that taught me how to save money so that I could always keep an accurate accounting of what money was for what item.

How to Save Money: The Virtual Envelope System

In essence I made a virtual envelope system by creating savings categories and assigning each category a name. Some of the money management apps that are available today have this feature built into them. I’m a bit old school having started this process using an Excel spreadsheet years ago. It has worked so good for us that I haven’t stopped using it.

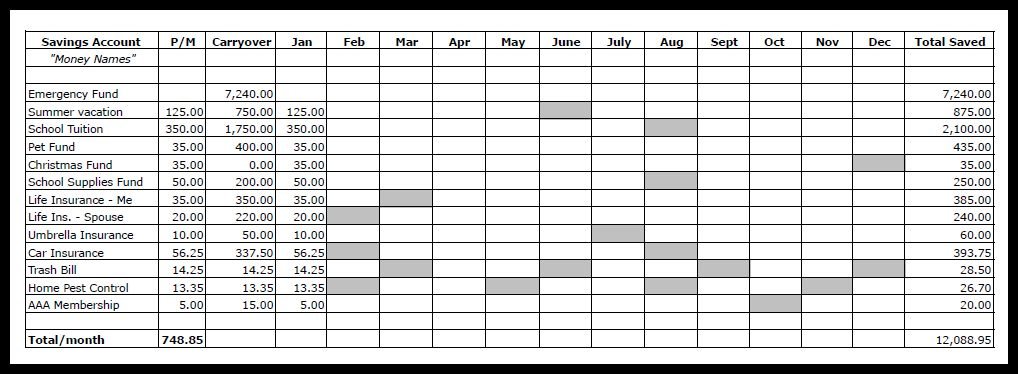

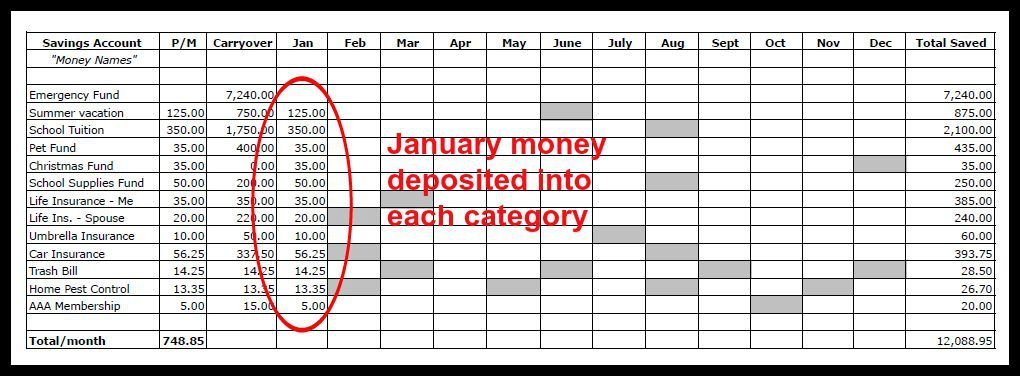

Below is a sample savings spreadsheet like the one I use.

My Process

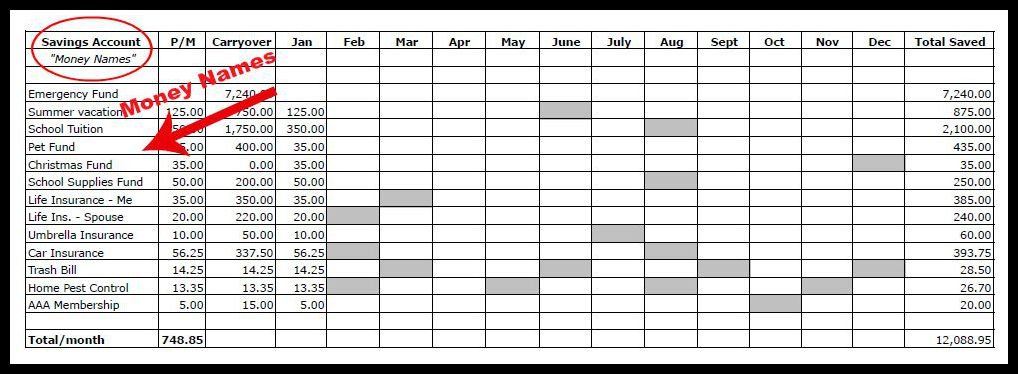

As you can see, I’ve labeled the far left column “Savings Account.” The categories listed on the lines under this are the items we are saving for. I’ve given each one of them a name. This specific name gives me clarity for what I’m saving for.

Giving each saving category/item a name is a must. Otherwise money gets lost in the shuffle. You won’t really know how much you’ve already saved for any specific item unless you separate it this way.

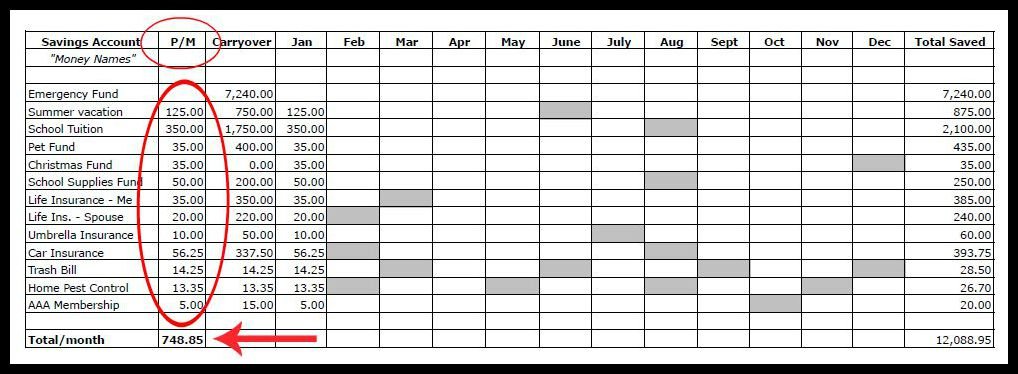

Column two on the spreadsheet is labeled “P/M” which stands for per month. This is the amount of money you would intentionally deposit every month into each category. When added up in this example it comes to $748.85.

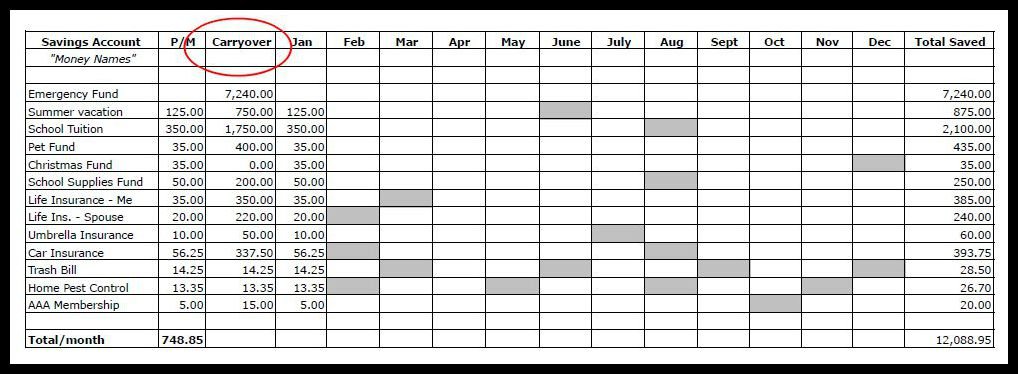

Column 3 is labeled “Carryover.” The amounts listed there reflect what had accumulated in that category during the previous year. I manually transfer that amount from the prior year’s saving spreadsheet so nothing gets lost in the yearly transition to a new template.

You will then notice each month has been given a column. On this example we’ve already deposited our $748.85 for the month of January.

As you deposit money every month, the “Total Saved” on the far right column will increase. You can enter this manually or use an Excel formula that automatically adds all the cell numbers in a particular row.

All the individual category money is totaled at the bottom. That number should correspond to what is in your bank. All the money in your savings account at the bank is accounted for here.

Final Spreadsheet Notes

A couple of final notes on the spreadsheet to point out. The grayed out cells indicate to me the month I know the bill is coming or when the money will be needed. That will of course vary for every person. Once you use the money during that month, you have to adjust what cells are added in the “Total Saved” column to reflect that some money has left the savings account.

If you take money out for any reason, just enter that into the cell as a negative number. Then either subtract it from the “Total Saved” column or let the formula do its work.

Personalize Your Savings System

I know this will click with some people because your brain is wired like mine. It may seem overwhelming but it’s really easy to set up, even for someone who is a novice at spreadsheets.

For others, a spreadsheet is the last option you’d use to keep track of your savings. For you an app works best. Many use a software program like Quicken. That’s completely fine. Find a system that works best for you and use it consistently.

Learning how to save money the right way isn’t difficult. It just takes planning. The best way I’ve seen on how to save money without losing track of what it is for is by designating categories this way. It creates discipline for me. I’ll be less likely and less tempted to use the designated money for something else.

If you like this method to keep track of your savings categories, I’m providing you with an Excel template which you can download. It’s already coded with the proper formulas to automatically add the rows and columns as you enter data. You can plug in your own categories in the “Savings Account” column and add more rows as necessary. Right click where you want to insert a row, click “Insert” and then select “Entire Row”.

If you have any questions about this please email me using the Contact Form. Happy (and organized) saving!

Leave a Comment or Answer a Question Below: Have you ever had problems keeping track of all the things you are saving for? Did you ever use money you were saving for one thing for something else? What method to you use to keep track of all the items you are saving for? Was there another system that taught you how to save money?

{kind=link}

Great Post Brian, I love spreadsheets and have built many for investing, but dont have any for budgeting. I’ll have to download yours. The only ‘spending’ spreadsheet I’ve created is to track real estate investing expenses. Thanks for sharing this!

No problem Jim. I’ve used that spreadsheet I created for years and it’s really helped us plan for those future expenses. Use my contact form and email me if you have any questions about the template.

Glad to see I practise most of those! For me the biggest headache was my car. I was in a minor accident 1 year ago but it was a blessing because I realized I didn’t need it. I don’t plan on getting another car, I’m saving so much money especially by not paying for gas, but MOST of all I feel so much more free! Less is more, and without the materialism or excess “stuff” you “think ” in our lives you realize you’re much more happier and peaceful. I walk more, bike more, and living a life of minimalism now.

A lot of times people try to preach one size fits all budgeting strategies. I like how you ended this one. Because it is important people know to pick what works for them or it can be a very painful process!

Thanks Brian another great post.

I use this simple spreadsheet to track my spending and savings. I also use envelope system, but it happens most of the time that I use an envelope for a different purpose because there are cases that come up unexpectedly.

This is exactly what I do too, although it is even more oldschool. I keep it written a sheet on our fridge. Every payday when I add to each category, I manually update it on the sheet. I actually find it really fun and rewarding. And it helps me stay totally clear on how much money we have for each category!

“…stay totally clear…” That’s the big goal of any system. I want to know exactly what I have going in each category. And like you I find it really fun to keep track of. Does that make us weird? 🙂

I’ve used an automated version of the “envelope system” and it’s a great way to physically see where your funds are earmarked. It’s kind of like an at-home system of fund accounting.

We don’t currently used targeted savings accounts, but we did for about five years. We went with the other interpretation of how to digitize the envelope system - multiple savings accounts at one bank. I think at our peak we had 13 savings accounts with Ally. I still tracked them with an Excel spreadsheet, actually, but they were separate buckets.

I think we will return to using targeted savings accounts. We still have a few in place - Charitable Giving, Taxes, Emergency Fund, and House Down Payment, and I like that they are siloed. But if we return to saving for short-term goals and expenses using targeted savings accounts, I’m not sure if I would open multiple accounts again or use your system of one account with multiple tracked purposes. They seem quite similar, since I was tracking the separate accounts, anyway. Without the discipline to track, I think having the multiple accounts is more clear.

We are actually using separate accounts - that way there is no denying that there is no money in the vacation fund, but there is money in the emergency account fund. We have always noticed a tendency of ours to check an account balance, versus a budget sheet, to see where we are at.

Good point Kirsten. I can see having a separate bank account for an emergency fund, maybe even one that is online that might earn a bit of interest. We have considered that. Beyond that I think one account is fine if you have a system for dividing everything down into categories.

This looks like a great system. I’ve often thought of creating something similar as I do not currently differentiate at all within my savings. I have one account that holds all of my savings, and it is large enough that I know I could afford to pay all of my yearly expenses even if they came due at the same time (which they don’t). I do like the idea of having targeted accounts for specific items, like travel or gifts, which would help me see more clearly if I’m spending more than anticipated in a certain area.

“…help me see more clearly if I’m spending more than anticipated in a certain area.” That’s an important consideration Ali that I should have mentioned. If we have saved “X” amount for an item (like vacation) then that helps limit what we spend…no going over that amount.