Is a high credit score really just a measure of how much you love debt? Seems like a tough question especially when you put the words “love” and “debt” right next to one another. I’m sure you are cringing right now just reading that.

Is a high credit score really just a measure of how much you love debt? Seems like a tough question especially when you put the words “love” and “debt” right next to one another. I’m sure you are cringing right now just reading that.

The financial services industry pounds the table on how to have a high credit score. In fact, I’ve read in multiple places online that a high score is “crucial” to one’s financial success. Without one you can’t get ahead and live the life you want. Hmmm…interesting.

So what does a high credit score look like?

Scores range from 300 - 850 with anything over 700 being considered a good rating. Excellent level ratings kick in around 750. The higher the score the more likely a lending institution will consider providing you with a credit card, mortgage or other loan.

In a credit driven society a high credit score seems like a must. The only problem is that to get a high credit score you HAVE to go into debt and stay in debt over time. There really is no way around that fact.

How Is A Credit Score Calculated?

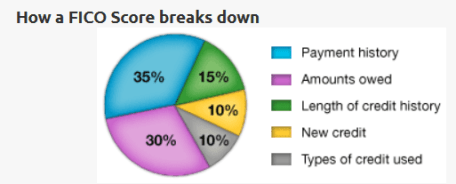

Credit scores take into consideration five categories as this image from MyFico.com shows:

Courtesy of myfico.com

As you can see, we have Payment History making up 35% of the equation. Essentially this examines how you’ve managed to pay your debt over time. A person can positively impact this piece of the pie by paying their debts on time.

How much a person owes in total accounts for 30% of the score. In other words, how much debt you currently have.

How long you have been in debt accounts for 15%.

The types of credit you possess (mortgages, credit cards, retail accounts) will make up another 10%.

Lastly, 10% of the equation is attributed to any new credit you have managed to acquire. Opening too many new accounts in a short period of time may negatively impact your credit score.

When I look at how a credit score is calculated, I see every single component in the equation is related to debt. The only way to attain a high score is to have a long credit history and pay off that debt consistently and on time. Then when those debts are paid, take out new debt so that you can pay that off on time. And on and on the cycle will go.

There are no points given for paying off all your debt and then staying out of debt, which is the path my wife and I have chosen. Pursuing that lifestyle will result in your credit score declining. I used to have an Excellent rating in the upper 700s. Since we quit using credit cards, paid off our mortgage and have no other outstanding loans our score is now below 700, which is only a fair rating. My credit score is being penalized because I’m no longer pursuing any debt obligations.

I guess it’s theoretically possible for it to go to zero now that we are managing our lives this way and only using debit cards and cash for payments.

And quite honestly I don’t really care if it goes to zero. We will not be taking out any loans in the future.

So in your pursuit of a high credit score are you secretly saying “I love debt?” I think a case could be made for that based on what’s factored into the equation.

Questions: Do you think a high credit score reflects how much you love debt? Are there other reasons to have a high credit score other than access to loans? For someone living a 100% debt free lifestyle is there a downside to having a low FICO score?

Original image courtesy of Jetske19 at Flickr Creative Commons

Next Post: Proof It’s the Thought That Counts

Prior Post: My Parents Were Frugal But Sometimes I’m Not

I’ve always thought this was kind of weird too. The game seems to be counter-intuitive, and one that’s probably not worth trying to “win”.

We encountered this bizarre conundrum when we bought our first house 2 years ago. We have no debt and we’ve never had any debt, so, while our credit scores were fine, the bank could not figure us out. I thought not having any debt was a reflection of how responsible we are, but the bank saw us as somewhat untested loan recipients because we hadn’t ever had debt. It was odd. But, we got our mortgage and bought our house and our credit scores jumped up! Having debt secured by property was apparently a great way for us to boost our credit scores 🙂

It was one of the unexpected and nice benefits of paying off a bunch of debt that our credit score got a very nice boost out of the whole affair. 🙂

Do you have any more debt to pay off? If not, expect it to begin to fall over time unless you are still paying off a mortgage or using credit cards.

Isn’t it Dave Ramsey who said it didn’t matter if his credit score went to zero, and I think you are obviously in that same camp. I think you are such a minority in our society that there really isn’t system for people who will never have debt. I guess if you don’t ever need a loan, it wouldn’t matter. I do believe car insurance is tied to credit scores, so you might have to appeal if your rates went up because you have no debt and don’t have an active credit score. It doesn’t seem fair to be penalized for doing all the right things financially.

“…there really isn’t system for people who will never have debt.” And in reality I’m not sure there has to be. We’ve chosen to live off the grid so to speak in regard to taking on debt.

What an interesting perspective. I never thought about that way, but yes your credit score really is “rewarding” you for taking on debt, paying it off and then taking on more debt again. It’s a vicious cycle now isn’t it. The worst part about it is how many people fall for the idea that you “need” to have a high credit score, so they take on debt (sometimes unnecessarily) to raise their score.

“…you “need” to have a high credit score…” You nailed it Kayla…that is the most deceptive and frustrating part of this whole issue to me. The idea that you cannot have a good life and get ahead financially without a high credit score is ludicrous.

Lots of great points, Brian. It’s hard because credit scores carry a lot of weight these days and affect things that you wouldn’t necessarily assume they would, such as getting a job. Maybe at a financial-related job, but I heard even grocery stores were running credit checks. It is not always an accurate picture, especially if someone, like yourself, chooses to not use credit cards and has no other loans. It’s definitely not a perfect system.

Grocery stores doing credit checks? That seems like an odd thing. Wonder what that is all about?

I’m not sure if having high credit score will help you in the long run. Maybe when you’re trying to get a mortgage or a loan. Just as you pointed out, having a high credit score just means that you love debt. If you are in debt and can’t get out of it, it really doesn’t matter how high your credit score is. You’re in trouble!

Well if you can’t get out of debt because you are late on payments or building up massive credit card debt then that’s going to negatively impact the score. So in that scenario it wouldn’t be high anyway. And you are right…you’d be in trouble! 🙂

It is pretty sad that the credit bureaus rely on debt to get your credit scores. We can all agree that there’s gotta be a better way, but determining which is the better way and how to implement it might be a little hard.

I don’t see it ever changing…there is too much money at stake.

It does penalize good people but if you don’t measure how people pay off their current debts how can you assess their future ones? I think there needs to be a better model that rewards people who have paid off major purchases and choose to be credit card free. That is a major accomplishment and shows a long history of dedication to living debt free. However this is one of the reasons we have a credit card is to maintain credit.

“…a better model that rewards people who have paid off major purchases and choose to be credit card free.” That’s actually a good distinction you raise Lance. I could choose to live credit card free but still require a loan for say a house upgrade (the only type of debt I would ever consider). If I hadn’t been paying on any debt recently my ability to secure that loan would be compromised.

Hi Brian,

Even if you aren’t using credit for debt it sadly still matters. It is one of the factors insurance companies use to give you an “insurance score” in which they decide the rates to charge you. I wish it didn’t matter if you didn’t have debt, but sadly it does.

Yeah, I had heard about credit scores impacting insurance rates. That’s really too bad. Those two industries should not be in cahoots. I’m going to check with my insurer to see how this is impacting me.

Our credit score is 820 -give or take a point or two-and we have zero debt. We do use credit cards and pay them off every month. So I would say that it is not a measure of how much we love debt.

It’s really a semantics argument as to what you consider debt. I’d say once you swipe that card you are in debt to that merchant, even if it’s just for a couple of weeks until the statement comes due. But I know many don’t see it that way.

I think there is definitely a weird dynamic with credit scores and the amount of debt you have at your disposal. My parents paid off their house a few years ago and closed down their credit profiles because they were scare of identity theft and when they checked their credit scores a few years ago, they were horrific. It’s weird that they could have a bunch of cash and no debt and have “bad” credit.

“…that they could have a bunch of cash and no debt and have “bad” credit.” Yeah, that’s funny…They could pay cash for a new house but couldn’t get a loan to buy the same house. Gotta love it! 🙂

YES! This is what Dave Ramsey talks about all the time. I couldn’t agree more on this. Really, my credit score is in the back of my mind. I have a good one b/c of my student loan debt, but when that’s gone, it is definitely not my main concern. I am not going to be in a relationship with debt forever. It’s just not for me.

Back when we had loans and credit cards I was consumed with it. We were doing all we could to make sure it wasn’t damaged. I remember feeling very proud every time we checked and it had gone up. Now I’m feeling proud that it’s going in the other direction.

I had no idea that high credit score was related to debt. I have been out of consumer debt for a long time and haven’t noticed a drop, so it’s something I’ll have to keep my eye on. I thought it was using credit responsibly that gave you a high credit score.

It does take into account all those consumer debts you paid off. Now it’s probably remaining high because of your good history and in part because you are paying off your credit card bill each month on time. There’s a more detailed analysis of it here: http://www.myfico.com/crediteducation/whatsinyourscore.aspx.

From my perspective, using a credit card does equate to going into debt even if it’s for a few weeks until the statement comes due. I know some might not agree with that way of thinking.

I don’t know that I completely agree that having a high credit score correlates to how much you love debt (because I know I don’t love it) :), but I definitely see your point. The only other point I can see where a high credit score can benefit you is if it begins to impact rates on things like auto insurance and stuff like that.

That said, I think this just goes to show again how skewed the credit scoring model is. It doesn’t reward those that are living a financially wise life that don’t use cards/loans for one reason or another. Be that someone just starting out but still financially prudent or someone like you & Kim that have killed your debt and are committed to that. I know it’s skewed, but I still think it’s crazy your score has been impacted by sort of going off the “grid” as it were. That just goes to show us again that it’s not a perfect system

I’m poking at people a little bit today with this just for fun. 🙂 Really want people to see and think through how the credit score is calculated and that the only way to maintain a high one is to continually have a line of credit open. For those that will be choosing to take out loans in the future there is no other way around it.

The system is definitely not rewarding us at the moment but that’s our choice I guess. I’d be interested at this point just to try and get a loan to see how hard it might be to qualify based on our current score.

That’s crazy! I can’t believe your credit score actually dropped since you stopped using debt!! How backward is that?? Although I guess if you are not planning to take on any additional debt it does not really matter, but still I think it would bother me to see that. But that’s probably the lifelong A student in me talking :-). Good for you guys for getting out of debt and staying out!

“…credit score actually dropped since you stopped using debt!!” That’s how the system works. Play by the rules or you lose. Well, in my case I consider it winning. 🙂